I always struggled with double-entry accounting, even after I got an MBA. I could do it and mostly memorized my way through a lot of the jargon, but it wasn’t until I took a systems view to accounting that I really understood the mechanics of how things worked. I figured I’d share some thoughts about that.

Stocks vs. Flows

A common theme in systems thinking is the idea of stock vs. flow. In accounting, everything looks like numbers, but in reality, some of those numbers are stocks, and some are flows, and understanding that distinction is critical.

So—more generally—what are stocks and flows? The classic illustrative example is a bathtub. The stock is the amount of water in the tub. Flows are water going into, or out of, the tub (via the drain and via the faucet). There are a few important relationships between stocks and flows:

- Time: A stock is measured as an amount at a fixed point in time (10 gallons at 10:00AM). A flow is actually a different unit, it is either a flow (ie 1 gallon / minute) or a fixed amount over a period (5 gallons between 10:00AM and 11:00AM).

- Space: A stock is measured for a system with a boundary (e.g. a bathtub). Anything within the boundary is part of that stock. Flow happens between system boundaries.

There is a simple law that holds true for all systems, which is that the change in stock of a system between two time periods is equal to the sum of the flow that happened within that period. This is obvious but stating it is important. If the tub had 10 gallons at 10:00AM and 15 gallons at 10:15AM, this means the total flow was +5 gallons in that period. It could be that the faucet added 10 gallons, 8 went down the drain, 1 evaporated, and you poured in 4 using a bucket. That sum has to be 5 (15 – 10).

How does this relate to personal finance? Well the first and obvious mistake is mixing stock and flow. Your cash balance, in a checking account, is a stock. An expense is a flow. They both look like numbers with a dollar sign, and they are related (like any stock and flow might be), but they are really different things.

Confusing stock and flow can often lead to simple mistakes or underspecified statements. Like “I have a $10K balance in my account in October”. That is an underspecified statement. Does it mean you maintained a minimum balance of $10K in October? Does it mean you had $10K at midnight of October 1st?

System Boundaries

One of the interesting pieces of systems thinking is that you can draw arbitrary boundaries around pieces of a system, and when you do, events can look very different. You can draw smaller boundaries to observe things more carefully, or larger boundaries for a broader view.

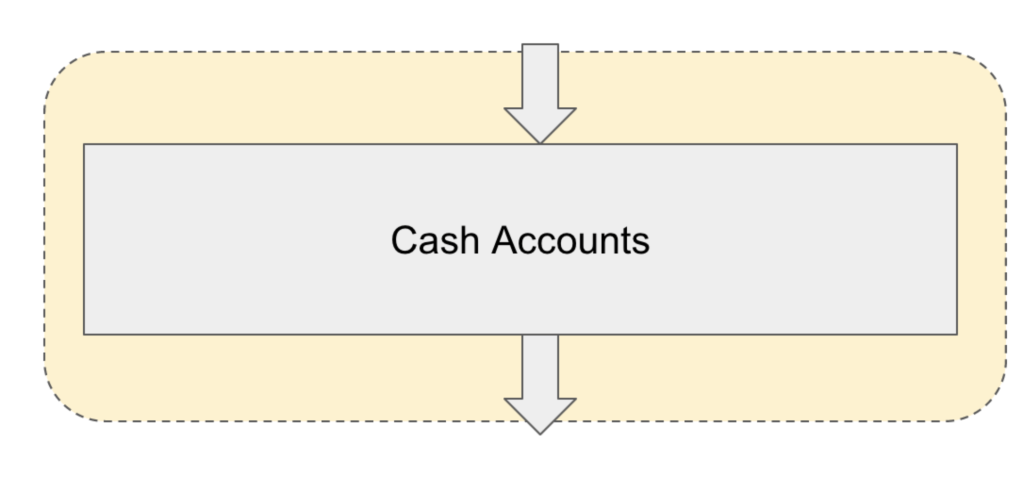

Let’s take this “system” with two cash accounts.

The green boundary encompasses only one account. That account has a balance, and it has some flows (cash flow). For the purposes of the green system, it doesn’t matter if a flow is an expense, a transfer, etc, all that matters is how big it was, whether it was in or out, and when it happened. You can call it a credit or a debit—that’s just convention.

A bank’s statement tells you the stocks and flows. For a period of time, the green “system” will have a starting balance, some flows (in and out), and an ending balance. That should all sum up.

In fact, if you know (or can predict) all the flows, you can derive the balance at any point in time. An account is a series of financial flows (magnitude, direction, datetime). The balance is always directly derivable from the cash flows. Simplistically, having that series of flows fully specifies the account. And, for the purposes of a single account, it doesn’t really matter where the money is flowing to (or from), just that it is flowing in (or out) of that single account.

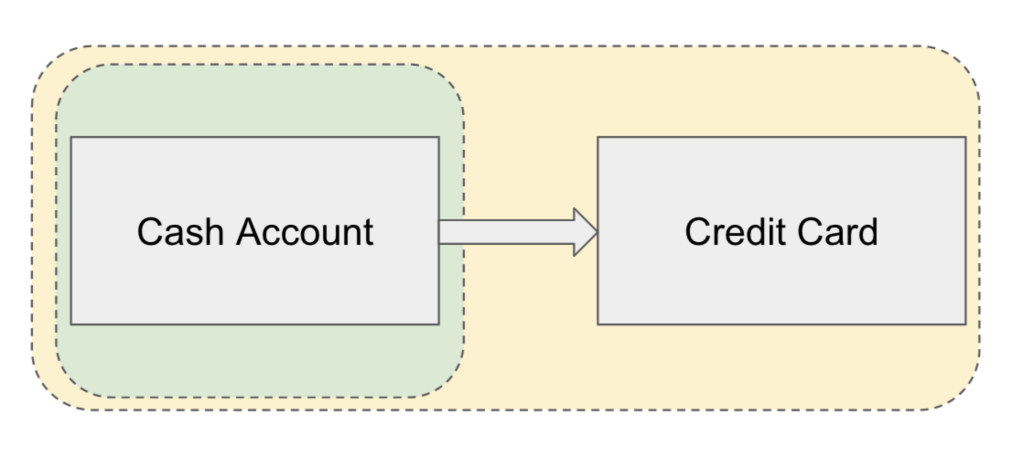

Now instead, if you take the (broader) yellow system, the story is different. A transfer between two accounts isn’t an inflow or outflow, it’s neutral, and you could, if you didn’t care about individual account balances, simplify the system like this:

Let’s do a slightly more complicated example. At Monarch, we sometimes see users treat credit card payments as an expense, while others treat them as a transfer. This discrepancy is pretty easy to explain using system boundaries.

If you’re using the yellow boundary, that payment is a neutral transfer. That’s also the proper accounting solution, of course. Technically, that payment doesn’t affect your net worth, because it reduces an asset and a liability by the same amount. It is two opposing flows.

But if you’re looking at the cash account only, because you’re cash-oriented (maybe because you’re worried that if you run out of cash you won’t be able to pay your rent or buy food), you’d be looking at the green boundary. In which case, that credit card payment is an outflow, and it looks more like expense. So, in a sense, while the yellow boundary gives you the right solution technically, it’s hard to tell someone looking at the green boundary that their explanation is wrong.

And in fact, the allocation of money within accounts does impact the future flows, in ways that people underestimate… because things like interest create a feedback loop, where future flows depend on the balance, and interest compounds in ways that people tend to always underestimate but is extremely poweful.

Let’s do one more, where you make a payment towards your auto loan.

If you take the green boundary, then a payment to your car loan looks like an outflow of cash from your account, and it seems like it is decreasing your net worth (ie an expense). However, if you take a broader system view, then you are actually paying down a liability, so your cash account is losing cash, but part of that cash is going to decreasing your liability (ie a transfer), and that part is neutral to your net worth. Then there’s interest involved too, but that interest is actually expense. And payments may have tax implications as well (e.g. mortgage). And of course, I didn’t even factor in that your car is depreciating. Anyway, the point is, a flow or event can look very different depending on how you draw your boundaries. Not only can it get more complicated, it also just looks like a completely different event.

Double-Entry Accounting

Double-entry accounting is the main paradigm in use with modern accounting. It sound scary—this is where you run into words like “debits” and “credits”. You can memorize what each of those is, but I find it a lot easier to first intuitively understand what’s going. And the stock and flow system model can help with that.

Double-entry means that every transaction to/from an account has to have corresponding, opposing entry to/from a different account. It’s not entirely intuitive to most people, but we can easily map it to our model by just creating the right system of accounts and drawing the right boundaries. Basically, because a transaction is a flow, it has to flow from somewhere (one entry) to the other (the other, opposing entry).

For example, a transfer between two bank accounts is easy, because the opposing transactions are clear. -$100 out of your checking account, $100 into your savings.

What about an expense? Expenses look something like this:

When you buy groceries for $10, you can think of it as being a flow of -$10 out of your cash accounts, and a flow of +$10 into a “groceries account”. Except the groceries account isn’t a “real account”, it’s just created because it helps us “balance the books”. And we shouldn’t include it inside our system boundary for net worth (or cash or anything else). But if you want, you could create a system boundary that encompasses all expenses, and it would look like this:

Businesses all use double-entry accounting. When they buy something, if that thing is an asset, they’d decrease their cash account, create an account for the new asset (or put into an existing asset account). They would then depreciate the asset over time (by, you guessed it, creating a “depreciation account”). The asset account is included in the business’s “net worth” (balance statement)—it’s inside that system boundary. But depreciation is outside the boundary, and so it isn’t, and it becomes an expense. (Of course, if they buy something that doesn’t become an asset, it would an immediate expense).

You can really create accounts for anything you want, and if you wanted a complete system, you would do exactly that.

Anyway, stocks and flows and double-entry accounting are the same thing, assuming you’re labeling things correctly, and all flows are opposing. The only difference is rather than using diagrams like we use in stocks and flows, a double-entry might look like:

I find stocks and flows more intuitive than double-entry accounting. For one, anyone I know who has studied accounting initially struggles to understand a debit vs a credit. Also, it’s less visual, and makes it less clear what the “system boundaries” are.

Going Beyond Simple Systems

Since we’re building a personal finance platform, we spend a lot of time thinking about these things.

Let’s assume you’re a person or household, and you’re trying to understand your financial picture. If you look at what a lot of current budgeting apps do, they provide:

- Historical views (spending): you can break things down by account, category, etc because you have the account-level data from banks. You can tell someone what they’ve spent money on. Sure, there might be some confusion around whether paying down a credit card is an expense or a transfer, but those are easily resolvable.

- Current views (balances): again, you can break things down pretty well if you have the account-level data. You can track balances and things like net worth over time, assuming you have the data and are tracking all accounts.

- Forward view (budgeting): this is where things start to fall apart, because this is where system boundaries start to matter a lot more. Most budgeting views take a really broad system boundary view, where expenses are outflows, income is inflow, and transfers are neutral (since they are within the system’s boundaries). Accounts are mostly lumped in together.

You can’t really do accurate long-term forecasting or give people solid financial advice based on that. You can’t model. Sure, it lets you build a simple product, and that can work for some people, but most people we talk to end up in spreadsheets because they want to model. Let’s look at some of the information you lose when you draw such a large system boundary for a forward-looking view of finances.

Balance-Dependent Flows (e.g. Interest)

In our simple two-cash-account example above, without any interest, the allocation of cash between accounts didn’t really matter. In reality, interest complicates things because it results in flows that depend on balances. Cash in a high-interest-rate savings account increases due to interest (and vice versa for a credit card balance incurring interest). So the allocation of balances within the broader boundary does impact the actual flows, and you can’t just lump everything together without losing some information that is crucial for forecasting (compounding interest is a huge factor in the longer term). Allocation does matter.

Gains / Losses

Interest actually isn’t terribly complicated because it is largely predictable. Gains and losses are a lot more volatile. A stock portfolio could appreciate or depreciate, which means traditional (physical) systems analogies break down. The water in your tub never appreciates. You can’t mark its value up or down. Water has to flow in or out, whether it’s through a faucet, drain, splashing, evaporation, or your toddler deciding to pee in it while you’re giving him a bath.

Now you for many types of assets, you can’t accurately forecast gains or losses. You can make assumptions based on history or your forecast (ie a certain growth rate for a portfolio of stocks), but it’s just a forecast. And that forecast will depend on allocation (are you investing in high-risk assets? Index funds? A mix?)

Liquidity / Hard Fungibility

Things that are “fungible” are things that can replace each other. Due to liquidity, not all dollars you own are “fungible”, and not all balances are interchangeable

A dollar in cash is not the same as a dollar in retirement savings in your 401K which is not the same as a dollar of value in a home you own. Various balances might have restrictions about when they can be liquidated (like desperately selling a house or car), might result in losses / expenses if liquidated at the wrong time (eg, paying taxes or penalties for early withdrawal from a retirement account), or might have transaction fees associated with them. A lot of this information is important for the purposes of forecasting and planning, but the broad system view just sums these up to your net worth. It’s nice to see how your net worth is trending, but having $10K in your retirement account today doesn’t mean that money is spendable right now.

Soft Fungibility

In addition to “hard fungibility”, there is also “soft fungibility” (I made this term up, I’m sure there’s a more formal one). Soft fungibility is mentally-imposed—it’s some emotional value you as a person assign to an allocation of money. Some people call that “earmarking”.

Sometimes, money with the same liquidity is treated differently, usually because it has earmarked that money for some purpose. For instance, let’s say someone (a parent) has two checking accounts: one out of which they spend regularly, and the other where they are keeping money to buy Christmas gifts for their children. Now let’s say there’s a shortfall in their spending account, will they dip into the Christmas gift account to cover it? Many people won’t. They might, instead, do something seemingly irrational, like borrowing at high-interest to cover their spending, just to avoid touching this “earmarked” money.

In fact, there is a lot of research into why some people have savings earning low interest while carrying debt with high interest, when the rational thing to do would be to use the savings to pay down the debt. The reasons are complicated, but usually it’s because they have earmarked their savings for some purpose, and a dollar that has been “earmarked” for something seems to be worth more than its intrinsic value.

Putting It Together

So based on the previous few points, you might assume that to really master finances, you need to worry about really granular, detailed data. You need a full system, with internal and external boundaries.

And to some extent, that is true. But that introduces complexity. And while you can use software and good product design to hide some of that complexity, at some point, it eventually bleeds through—and the system stops being purely mechanical, because there are humans in the mix.

Humans with goals and aspirations for the future, but also concerns and worries. Humans with baggage and a complex relationship with money. Humans that might throw their hands up and avoid problems that seem complex or stressful. So there’s a balance between creating a system that’s complete, but complicated, and one that’s tractable, but misses big parts of the picture.

And there are ways to navigate that tension, using good product design, basic psychology, and—spoiler alert—systems thinking. But that’s a topic for another post.

(After writing this, I came across this excellent piece by the awesome Martin Kleppmann, which is probably a lot more eloquent than anything I’d ever write. But I still figured it was worth sharing the systems model, since it is slightly different)